HKSFC Tokenisation Circular: Key Stakeholder Takeaways for Secondary Trading of Tokenised Products

HKSFC Tokenisation Circular: Key Stakeholder Takeaways for Secondary Trading of Tokenised Products

MAY 7, 2026

HKSFC Tokenisation Circular: Key Stakeholder Takeaways for Secondary Trading of Tokenised Products

On 20 April, the Hong Kong Securities and Futures Commission (SFC) released updated circulars that clarify the regulatory framework governing the secondary trading of tokenised, SFC‑authorised investment products. Importantly, these updates preserve the existing mechanisms for primary subscription and redemption, ensuring continuity for market participants. This guidance provides crucial regulatory certainty, demonstrating how tokenisation can be effectively integrated into a well‑regulated secondary market. This formally allows secondary trading of tokenised products without diluting core investor protection whilst upholding robust investor protections.

What are the key stakeholder takeaways from the SFC’s latest tokenisation circular?

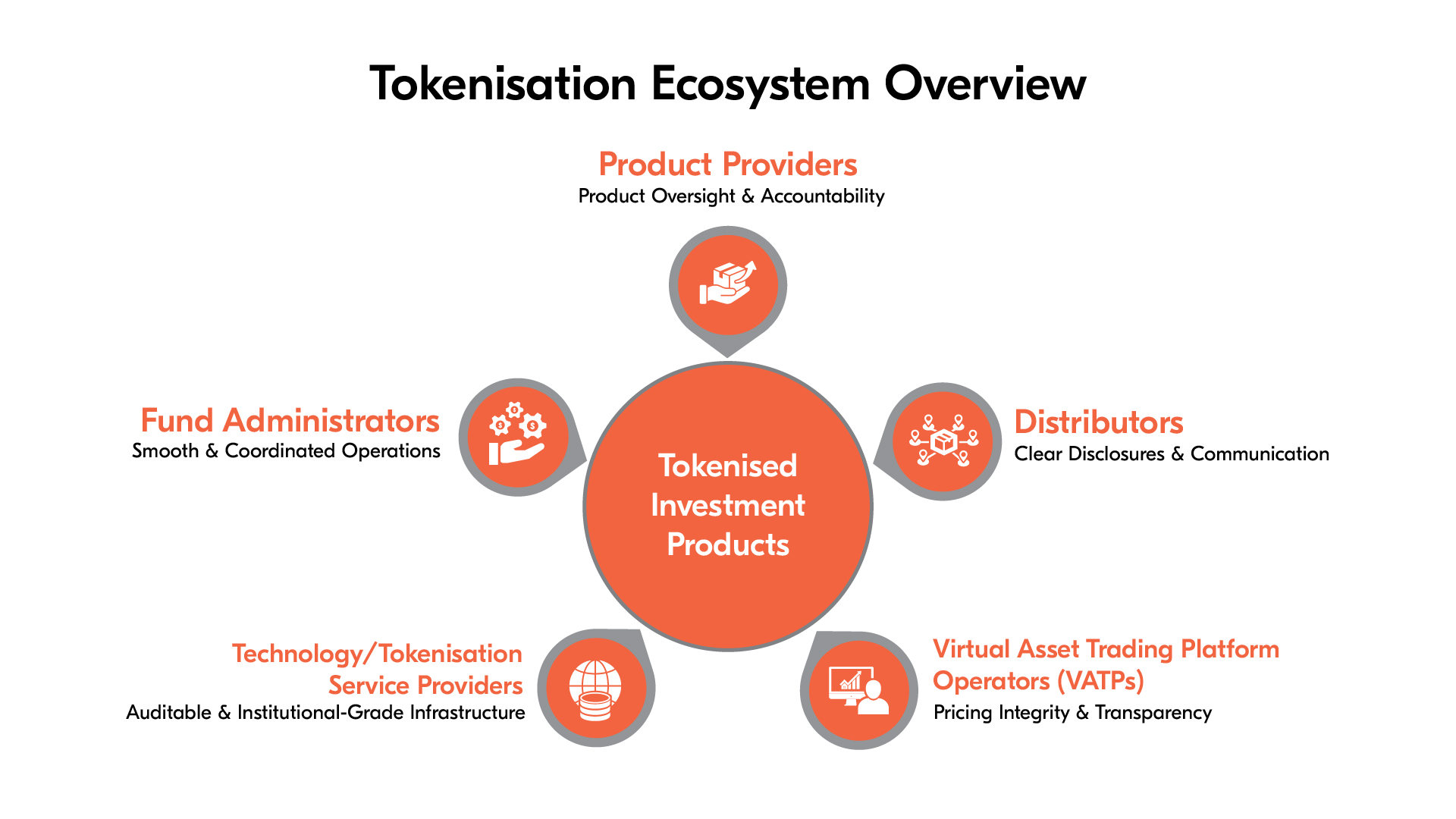

Product Providers

Product Providers

With tokenisation expanding distribution and liquidity, product providers are also further expected to implement better governance, operational readiness, and transparency.

Secondary liquidity is a managed outcome. Issuers are expected to proactively design, implement and continuously monitor liquidity and market-making arrangements for secondary trading.

Regulatory engagement is part of product lifecycle management. Providers are to have an early consultation and ongoing engagement with the SFC. This is critical not just at launch, but also for any material changes to tokenisation structures. Providers must implement escalation frameworks to immediately report material incidents (e.g. technology failures, disruptions in token ownership records or control issues).

Disclosure must evolve accordingly. Issuers must ensure that the offering documents go beyond traditional fund disclosures to clearly explain the available secondary trading channels, liquidity dynamics, price deviation risks, market making and potential trading suspensions or disruptions.

Primary market remains as the anchor of fair value. Providers must maintain robust primary subscription and redemption mechanisms at official net asset value (NAV), ensuring a reliable price preference. They must also enable efficient fungibility and transferability of tokenized products across primary and secondary markets, to prevent fragmentation between tokenised and traditional units.

End-to-end accountability remains with the issuer. They remain fully accountable for product governance, operational integrity and investor outcomes. This also applies to where tokenisation functions are outsourced to third parties.

Authorisation status is continuous, not one-off. Product providers must ensure that the underlying fund continues to comply with all SFC authorisation requirements.

Distributors

For distributors, tokenisation does not simplify obligations, but it adds a new layer of complexity. As they are required to have stronger client communication, clearer disclosures and more secure integration between traditional fund distribution and digital trading infrastructure.

Enable informed client choice. Distributors must clearly guide investors on the differences between primary and secondary trading, along with the relevant risks. They must ensure decisions are based on meeting client suitability, disclosure and investor-protection requirements.

Full compliance still applies. Tokenised products must be distributed under the applicable SFC licensing and conduct requirements.

Primary dealing remains core. Distributors must continue to process subscriptions and redemption requests, ensuring access to the primary market as the pricing anchor.

Virtual Asset Trading Platform Operators (VATPs)

VATPs are not just execution venues as they are expected to actively safeguard pricing integrity, liquidity and transparency. This forms the backbone of a credible tokenised secondary market, as they oversee making sure of:

Prioritizing fair pricing. Platforms are expected to implement fair pricing safeguards, such as price deviation controls and alerts where trading prices materially diverge from indicative NAV (iNAV).

Transparent pricing mechanisms. They are required to provide clear disclosures on pricing. This is important to distinguish that primary market transactions are based on official NAV from the fund administrator, while secondary market prices are market-driven and may deviate.

Actively managing market makers. VATPs must conduct due diligence and ongoing monitoring of market makers, including expectations on quoting, spreads and participation, as to guarantee consistent liquidity support.

Disseminating reliable NAV data. Platforms must disseminate timely iNAV updates and the latest official NAV data, with transparent data sources and update frequency to enable informed price discovery among investors.

Safeguarding Investor onboarding. VATPs must ensure appropriate risk disclosures and explicit investor acknowledgement regarding pricing, liquidity and market structure risks, before enabling secondary trading.

Full trading and surveillance standards. VATPs must apply existing trading rules, risk controls and market surveillance measures to tokenised products, covering both pre-trade and post-trade monitoring to ensure fair and orderly markets.

Technology and Tokenisation Service Providers

Service providers are expected to deliver institution-grade, auditable and regulator-ready infrastructure whilst operating under the full accountability of product providers. Being an essential part of the tokenised fund structure, they:

Operate as delegated infrastructure providers. Technology and tokenisation service providers may perform key outsourced functions, such as token issuance, smart contract execution and ledger administration, but always within a framework defined and overseen by the product provider.

Do not assume regulatory responsibility. Product providers remain accountable for governance, record-keeping and investor outcomes. This means that service providers must operate under strict oversight and clearly defined mandates.

Build for auditability, control, efficiency and resilience. The infrastructure must support accurate and verifiable ownership records to ensure that regulators and product providers can validate holdings at any time. Tokenisation systems should also incorporate access controls and transfer restrictions to align with regulatory expectations around investor protextion and ownership certainty. While solutions must allow for regulatory access, oversight, inspection and protection are essential to mitigate operational and technology risks.

Fund Administrator – Key Role in a Tokenised Fund Structure

Although fund administrators are not the direct addressees of the SFC circulars, they are just as critical to making a tokenised fund operate smoothly, especially around NAV, register integrity and operational controls. They play a central enabling role in ensuring tokenised funds operate with the same integrity as traditional structures, as they:

Anchor pricing on official NAV. Administrators remain responsible for producing the official NAV for primary subscriptions/redemptions and must align NAV timing and data governance with all stakeholders.

Enable transparency without pricing the market. By enabling reliable NAV/iNAV inputs and clear valuation cut-offs, administrators support informed secondary trading, without controlling secondary market prices.

Support controlled token lifecycle processes. Administrators play a role in mint and burn workflows, ensuring proper segregation of duties, validation and governance controls are established.

Coordinate cross-party operations. Effective tokenisation requires close coordination across product providers, distributors and VATPs. This includes data flows, cut-off times and exception handling.

Safeguard records and reconciliation. Maintaining accurate books and records is critical. This includes reconciling on-chain token supply with the off-chain fund share register to ensure ownership consistency.

Support onboarding and compliance as necessary. Where applicable, administrators may assist with investor onboarding, transaction processing and AML/KYC compliance checks for in-kind contributions.

How Can the SFC’s Tokenisation Circular Affect You?

The SFC’s framework clarifies that tokenisation is no longer experimental. It is already operational. However, success will depend on how quickly and effectively each stakeholder translates guidance into practice.

The latest circular significantly expands Hong Kong’s tokenisation framework from focusing mainly on issuance and primary dealing to now supporting a secondary trading ecosystem for tokenised investment products. Much greater emphasis is placed on secondary market liquidity, pricing transparency, market monitoring, investor disclosures, and coordination across all stakeholders.

Ultimately, the framework signals a shift from tokenisation as a limited operational feature to tokenisation as part of a broader, institution-grade market infrastructure. The opportunity is clear, but so is the expectation to move early, align closely with regulators and build with control, transparency and investor protection at the core. From here on, initial action and proactive engagement with regulators are key to staying ahead.

Partnering with Bolder Group

With the SFC’s updated circular now in effect, stakeholders must move decisively to strengthen governance, enhance disclosures and ensure operational readiness across both primary and secondary markets. As tokenised products are realised, stakeholders increasingly need integrated operational, governance, and technology solutions.

As an independent global service provider, Bolder delivers specialised, institutional-grade services for tokenisation and digital assets, bridging traditional finance with blockchain technology. Our team of experts offers an array of digital assets solutions to help you build early, build right, while navigating this next phase of tokenised markets with confidence.

Ready to begin building with us? Contact our Bolder representatives here to get started.