China Offshore Trust Tax: New Disclosure Rules for 2026

APRIL 24, 2026

For decades, offshore trusts were the preferred tool for China’s ultra-high-net-worth families to manage Hong Kong-listed shares and plan multi-generational succession planning. Long considered a safe haven with limited oversight and minimal reporting requirements, these structures now face intensifying scrutiny. The Chinese authorities’ tax enforcers are now targeting these structures.

Regulators in key economic hubs are demanding detailed, multi-year financial information disclosures. In some instances, local bureaus are imposing a 20% levy on investment gains, along with significant penalties. This highlights Beijing’s objective of boosting tax revenue amid an economic slowdown and fiscal strain.

Navigating a Structural Economic Shift

Faced with a widening fiscal deficit and a sluggish economy, China has intensified its focus on revenue collection. A key focus involves “red-chip” listings, referring to companies that operate in mainland China but incorporate offshore to list on the Hong Kong Stock Exchange. Notably, personal income tax revenue rose 11.5% in 2024, reaching 1.62 trillion yuan.

Authorities are now fundamentally re-evaluating how these red-chip firms use offshore trusts, with the China Securities Regulatory Commission (CSRC) implementing more stringent oversight to prioritise transparency. As a result, the heightened regulatory burden is prompting some founders to reconsider using trusts for initial public offerings (IPOs).

In 2025, China experienced significant capital flight, with an estimated $1.04 trillion in capital outflows exiting the country. In response, Beijing has intensified capital controls, including removing cross-border brokerage platforms from mobile app stores, to stem the tide.

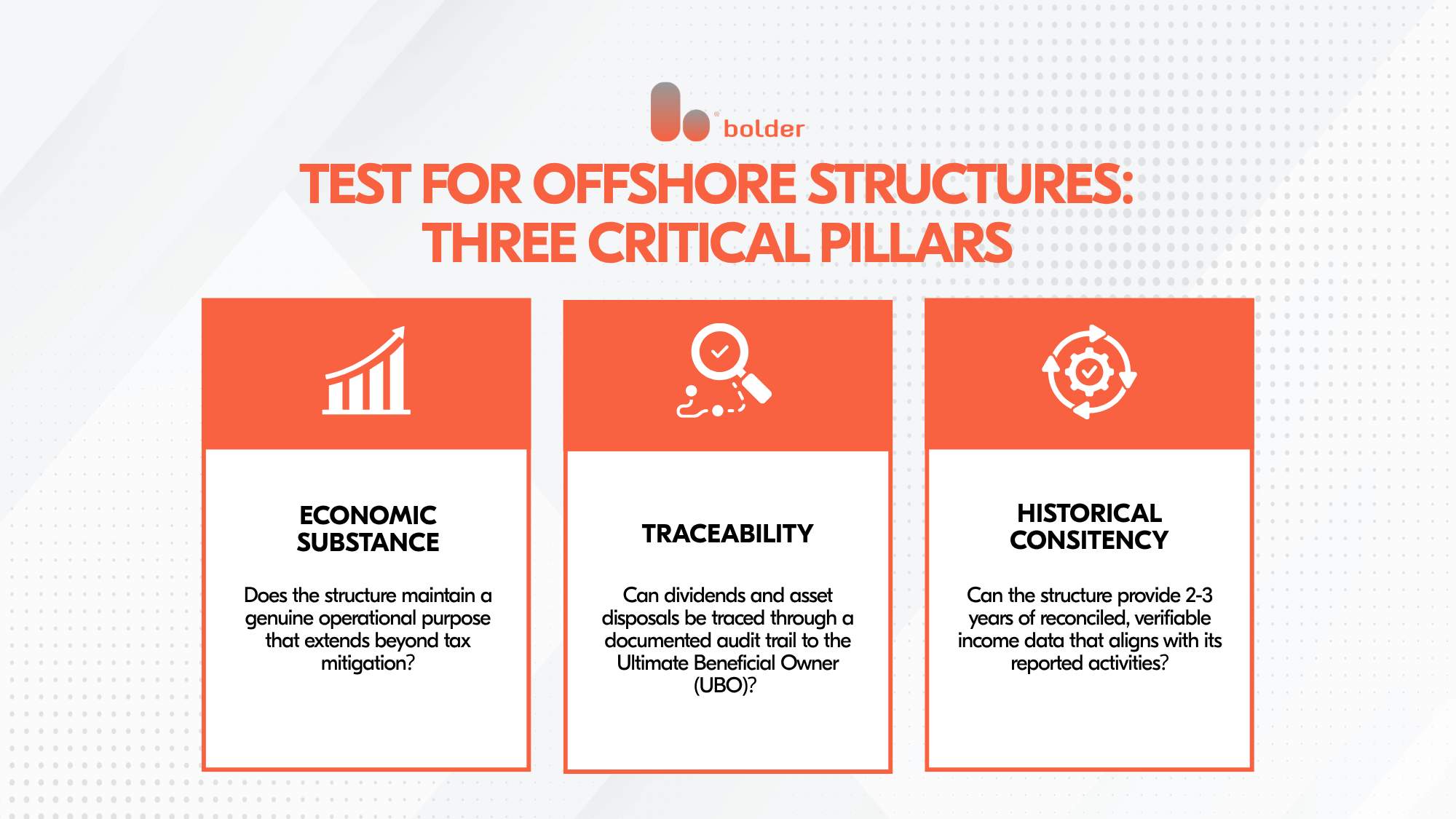

Passing the Economic Substance Test: How Does the Structure Function?

The regulatory benchmark today is straightforward: if an offshore structure can withstand a holistic review of its ownership, governance and reporting, while remaining transparent and consistent. Tax authorities are no longer focused solely on domicile considerations, but are placing greater weight on operational substance, ultimate beneficiaries and the credibility of economic outcomes.

To withstand a holistic review, an offshore structure must provide transparent answers to the following key questions.

Operational Discipline

Current market shifts should not be interpreted as a retreat from offshore planning. The challenge at hand is not jurisdiction, but a lack of transparency and operational oversight. As we move through 2026, legacy structures become increasingly fragile under global scrutiny. To ensure long-term resilience, these structures must adopt a disciplined process to institutionalise their governance and reporting standards.

This transition demands the evolution of private structures into institutional-grade frameworks. To achieve this, the following standards must be institutionalised regardless of the jurisdiction:

Robust Accounting: Unified, consolidated reporting framework that mitigates oversight risk.

Verified Governance: Clear role-based accountability for settlors, trustees and protectors to ensure compliance.

Defensible Rationale: Comprehensive economic documentation for all ownership structures to ensure a defensible rationale for every transaction.

Structures that meet these standards demonstrate structural durability, while non‑compliant structures inevitably encounter operational and regulatory friction, regardless of their domicile.

Hong Kong’s Strategic Role

Within this evolving landscape, Hong Kong remains a pivotal hub for cross-border structuring. It remains a rules-based jurisdiction distinguished by (a) clear governance standards, (b) defined financial reporting requirements and (c) the ability to administer structures with continuity and operational discipline. Moreover, Hong Kong remains a natural hub for families with international assets, bridging the gap between the traditional needs of private wealth and the institutional discipline increasingly required by regulators.

Looking Ahead

Offshore trusts may be undergoing a fundamental transformation, but they are not in decline. The industry is moving towards institutional-grade governance. In this new era, success is defined by well-governed ownership platforms—structures designed for long-term viability and to withstand modern regulatory scrutiny without operational disruption.

For wealthy individuals and business owners, it’s no longer about creating new structures, but about whether current structures can survive a holistic review without reconstruction. Proactive engagement allows families to streamline operations and reinforce governance. Meanwhile, those who hesitate may be exposed to jurisdictional and operational uncertainty.

Future-Proof Your Legacy with Bolder

The rapid evolution of tax transparency is driving the need for robust structural governance. Whether you are reviewing your current offshore structure or seeking an independent assessment to ensure it meets the demands of 2026, Bolder offers a high-level, confidential consultation to ensure your arrangements are both resilient and future-ready.

Our team of experts provides technical expertise and institutional discipline to ensure your wealth structures are not only compliant but also durable in the long term. Each solution is bespoke, tailored to the unique needs of each family, their assets and their risk appetite.

Ready to future-proof your offshore arrangements? Contact us today!